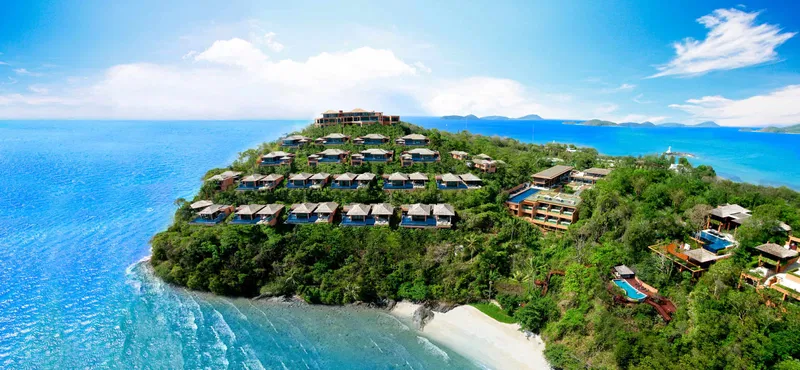

Sri Panwa Phuket

AI Verdict

out of 10.0

Executive Summary

Strong fundamentals across all categories. This project represents a compelling investment opportunity.

Price From

฿48.0M

Price / sqm

฿153,431

Foreign Quota

49%

This project scored well — talk to our specialist about next steps

Independent analysis · No commission pressure · Free consultation

Project Gallery

Score Breakdown

AI Research Disclaimer: All scores, assessments, and findings in this report are generated algorithmically by AI agents based solely on publicly available information at the time of research. They do not represent the personal opinion of Phuket Investor Hub, its owners, or any affiliated parties. No statement herein is intended to defame, disparage, or impugn the reputation of any developer, company, or individual.

ROI Potential

Weight: 20%

Projected return on investment based on rental yields, capital appreciation trends, and guaranteed returns offered by the developer.

Developer Reputation

Weight: 15%

Track record of the developer including past project delivery, build quality, financial stability, and market standing.

Location Quality

Weight: 15%

Proximity to beaches, airports, shopping, hospitals, and overall desirability of the neighborhood for both living and renting.

Funding & Delivery Risk

Weight: 15%

Assessment of construction progress, funding structure, escrow arrangements, and likelihood of on-time completion.

Legal Compliance

Weight: 15%

Foreign ownership structure (freehold/leasehold), EIA permits, condominium act compliance, and title deed status.

Value for Money

Weight: 10%

Price per square meter compared to similar projects in the area, included amenities, and furniture packages.

Resale & Liquidity

Weight: 10%

Ease of reselling the unit based on market demand, foreign quota availability, and historical transaction volumes in the area.

Full Research Report

Pricing Analysis

At an average of ~฿153,431/sqm, Sri Panwa is positioned in the upper-tier of Phuket's luxury market. While the absolute price points (฿48M+) are high, the per-sqm rate is competitive when compared to newer ultra-luxury branded residences in prime west coast locations (e.g., The Residences at Anantara Layan, Banyan Tree Grand Residences), which can exceed ฿200,000-฿250,000/sqm. The price reflects the established brand, proven operational success, and unique location. Buyers are paying for brand equity and a proven rental-performing asset, not just physical real estate.

Fee Structure

Owners must budget for significant ongoing costs. This includes: 1) Common area management fees (CAM), which are high due to the extensive 40-acre estate and 5-star facilities. 2) A share of operating expenses if in the rental pool (e.g., marketing, booking commissions, staff). 3) A revenue split with the hotel operator (e.g., 60% to operator, 40% to owner). 4) Standard property transfer fees (2% of appraised value, split between buyer/seller), stamp duty (0.5%), and specific business tax (3.3%) if applicable on resale.

Roi Projections

Marketing claims are not the focus here; the investment is based on the hotel's actual performance. A realistic net yield would be in the 2-4% range annually, after deducting all fees, management splits, and operating costs. This is a typical range for luxury branded residences. The primary investment return is weighted towards capital appreciation, driven by the brand's strength, the scarcity of private peninsulas in Phuket, and lifestyle returns (e.g., owner's usage entitlement, typically 30-60 days per year).

Market Comparison

Compared to villas in Laguna (Banyan Tree, Angsana), Sri Panwa offers more privacy and dramatic sea views but is more isolated. Compared to west coast properties in Surin or Kamala (e.g., Amanpuri), it offers a different vibe—panoramic bay views instead of direct sunset beach access. Its key differentiator is the vibrant, trendy 'Baba' brand identity, which attracts a younger, affluent demographic compared to more traditional luxury resorts.

Buyer's Guide: Purchasing Property in Thailand

This section provides general guidance for foreign buyers interested in Thai real estate. It is for informational purposes only — always consult qualified Thai legal counsel before purchasing.

🏠 How Foreigners Can Buy

- • Condominium Freehold: Foreigners can own up to 49% of a condo building's total area outright.

- • Leasehold: 30-year lease renewable up to 90 years. Common for villas and land.

- • Thai Company Structure: Some buyers use Thai companies, but this carries regulatory risks.

💰 Costs & Fees to Expect

- • Transfer Fee: 2% of appraised value (often split 50/50 with developer)

- • Sinking Fund: One-time payment (฿400-800/sqm typical)

- • Common Area Maintenance: Monthly fee (฿40-100/sqm/month)

- • Furniture Package: Often ฿200,000-800,000 depending on unit size

✅ Due Diligence Checklist

- • Verify the developer's EIA approval

- • Check the construction permit and building license

- • Review the Condo Act compliance certificate

- • Confirm foreign ownership quota availability

- • Review the sales contract with an independent Thai lawyer

- • Verify escrow account arrangements for off-plan purchases

⚖️ Risks & Rewards

Potential Rewards:

- • Guaranteed rental returns (5-7% typical for Phuket)

- • Strong capital appreciation in prime areas

- • Growing tourism market

Key Risks:

- • Off-plan construction delays or developer insolvency

- • Currency exchange fluctuations

- • Rental yield guarantees may not be sustainable long-term